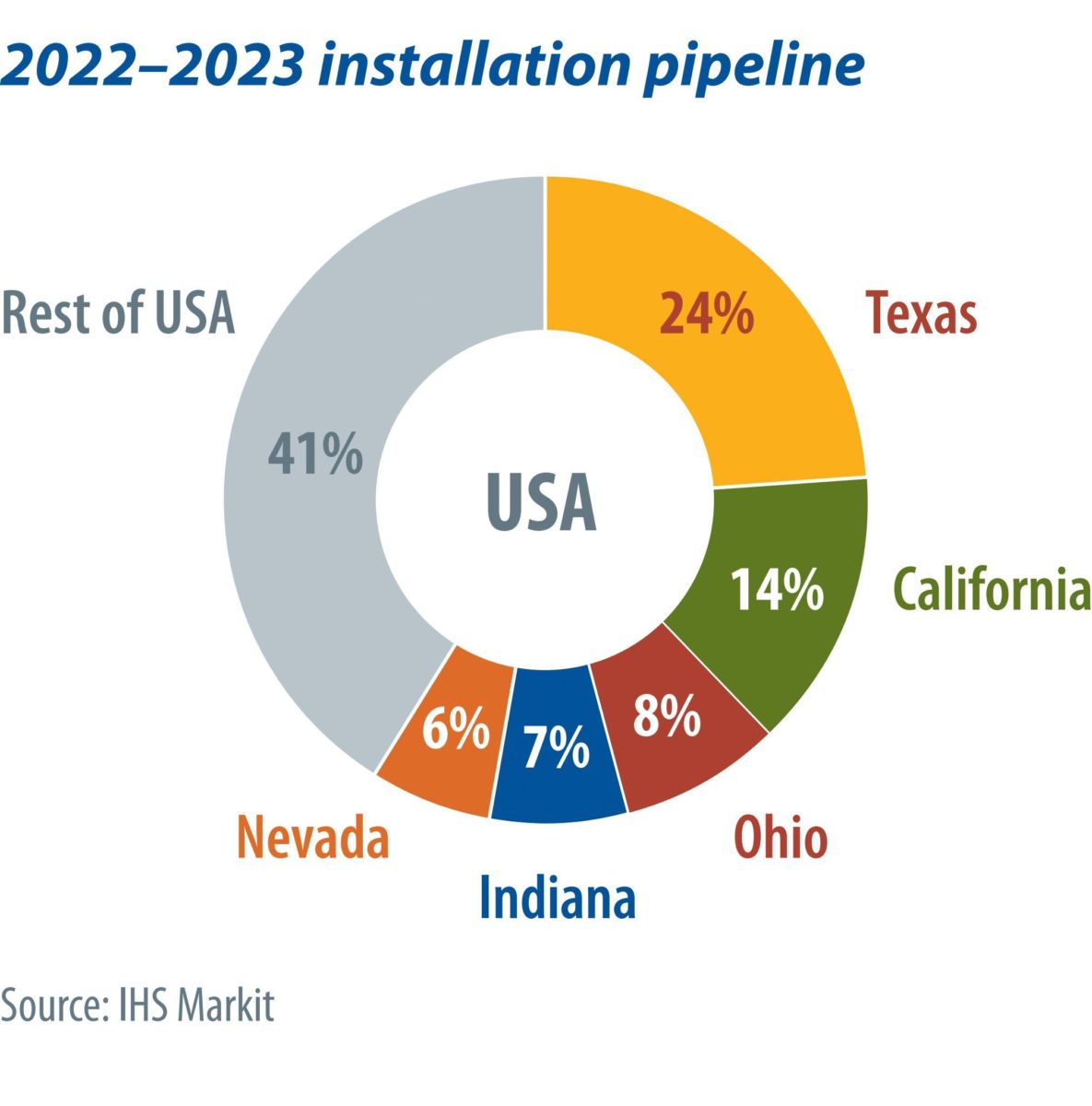

Next year will set new records for the U.S. solar market, with 30.4 GW of installations expected. The utility-scale PV pipeline in 2022 is nearly 50% greater than 2021 and 2023, due to the combined effects of pandemic-related supply chain impacts, the solar Investment Tax Credit schedule, and other module procurement challenges. Over the next two years, solar installations will be concentrated in Texas, California, Ohio, Indiana, and Nevada, with large portions of the pipeline being developed by a few key players in each state. IHS Markit’s Eric Wright takes a closer look.

"The 2022 pipeline for utility-scale solar projects planned for completion in the United States is nearly 50% greater than in 2021 and 2023."

Source: IHS Markit

Stay informed

pv magazine is the leading trade media platform covering the global solar photovoltaics industry. Log in or purchase a digital or print version of this issue to read this article in full.

The cookie settings on this website are set to "allow cookies" to give you the best browsing experience possible. If you continue to use this website without changing your cookie settings or you click "Accept" below then you are consenting to this.