In light of green hydrogen’s potential and the geopolitical prospectus of the 21st Century, a question arises: would the sun have set on the British Empire if it had been covered in solar panels? This is to say, if green hydrogen is going to power this century forward, which nation or nations will possess that power? Those with the key resources of solar and wind must now be engaged in a geopolitical race for that power both literal, economic and political.

Of course, fossil fuels can also be used to generate hydrogen. However, as Professor Ad van Wijk of TU Delft in the Netherlands explains, costs of green hydrogen are likely to fall. “If you can produce electricity for US$0.01-0.02/kWh, and in solar there are good signs already… then you can produce for $1.50-2.00/kg.” At that price green hydrogen produced by solar and wind will out-compete gray and blue hydrogen.

Major actors

Goldman Sachs has called green hydrogen a “once-in-a-generation opportunity” that it estimates “could give rise to a €10 trillion addressable market globally by 2050 for the utilities industry alone.” Given such economic potential, realpolitik tells us that, like nuclear weapons, whoever lacks a foothold in the green hydrogen economy is at a significant geopolitical disadvantage. But, just as the United States had the scientists in WWII, it is the countries with the right resources, infrastructure, and entrepreneurial zeal, that have the distinct advantage in the race for green hydrogen.

Many nations are rich in solar and wind resources, fewer possess the other requirements alongside. According to Nadim Chaudhry, CEO of World Hydrogen Leaders, an online platform of industry executives designed to accelerate the production and distribution of clean hydrogen, the leaders in the geopolitical race for green hydrogen are Australia, Saudi Arabia, and the North Sea nations – the Netherlands in particular.

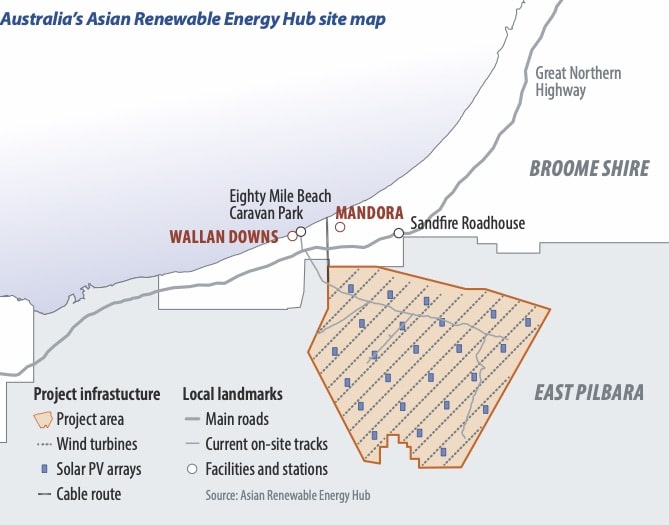

“Specifically, Australia” says Chaudhry, “for the sheer size of the proposed projects, political support, robust financial system with a low weighted average cost of capital, a strong body of entrepreneurs and the asset maximizing combination of wind and solar in say the Western Australian project of Infinite Blue Energy.” That project being the 26 GW Asian Renewable Energy Hub (AREH) in the Pilbara region of Western Australia (WA).

The AREH is not the only significant green hydrogen project in Australia, nor even in Western Australia, nor even in the Pilbara region. Proposals for green hydrogen plants are becoming commonplace in sunburnt and windswept Australia. In large part this is due to the interest of trading partners, particularly Japan and South Korea, but even a nation as far distant as Germany has joined Australia in a feasibility study for a supply chain.

Of course, there are countries far closer to Europe with similar resources, state-led economies such as Algeria, Morocco, and Saudi Arabia. However, Chaudhry suggests “they may lack the entrepreneurial pace of what is happening in Australia.” Like Wijk, Chaudhry says that it is a “race to scale and the costs of transport.” Green ammonia could prove a cost-effective energy vector in this regard, allowing a nation as far afield as Australia to reach extra-regional partners. Although, in the long term “Australia would lose any first mover advantage …There is lots of land in North Africa and four existing methane pipelines connecting Africa to Europe.”

Of course, we cannot forget the giant red dragon in the room. As Marius Foss, Head of Global Energy Systems at Rystad Energy explained, China are a race leader too thanks to “their willingness to invest heavily”, particularly in electrolyzers which Foss likens to solar manufacturing.

Citing Wright’s Law, Foss says that it’s “simply a volume game where the one that produces the most becomes the most competitive.” However, Foss also noted that if, as we are seeing in the battery space today, the United States and Europe develop “a willingness to pay a premium to get locally sourced components,” then China’s comparative advantage could deteriorate.

Bit parts

Given the logistics of transportation from resource rich areas to population hubs, it is hard to see the green hydrogen economy becoming monopolized anytime soon. As IDTechEX Energy Storage/Hydrogen Technology analyst, Daniele Gatti, told pv magazine: “Adopting a hydrogen economy means developing the entire supply chain: production, transportation and distribution, and also its consumption.”

Even Australia then, a big fish at this point, will ultimately have to settle for being a big fish in a regional pond – the Asia Pacific. “Australia will mainly have Japan, China, South Korea … as their home markets,” said Wijk. The world will be divided into regional markets of “cheap hydrogen where there will be competition purely on cost basis.” In Asia, for instance, Australia will compete with Saudi Arabia and Oman.

In a regional geopolitical landscape, there’s great potential for bit parts to play significant roles. Take Chile for example, in November 2020 President Sebastian Pinera set his government the ambitious goal of becoming one of the world’s leading exporters of green hydrogen by 2030.

According to S&P Global, President Pinera believes his country’s record solar irradiation levels mean it could become the world’s most efficient producer of green hydrogen, “more than compensating for the country’s distance from major markets.” However, considering the price of solar and wind will continue to drop across the board, in the long run Chile’s solar efficiency advantage wouldn’t obviate the transport costs incurred in its distance from major markets. In the end, Chile will be a big long fish in the American pond.

Among Chile’s green hydrogen competition in the Americas will be Canada. The Great White North has significant hydro and geothermal power. Such resources will not be able to compete for major market share with solar and wind but countries like Canada and Iceland can certainly produce green hydrogen cheaply.

This is not to forget the giant, until recently orange, dragon in the room, the United States. As Wijk pointed out, not even the Trump Administration attempted to diminish the growth of hydrogen. “And why was that?” he asked rhetorically, “Because you can also produce hydrogen from coal and natural gas.” Though it is hard to see the Biden Administration continuing in that vein, the United States suffers under the same transport costs as everyone else, and due to its natural gas reserves, like Russia, it will likely proceed with hybridized hydrogen for the foreseeable future.

Some potential dark horses in the geopolitical race for the green hydrogen economy, particularly from a European perspective, are Portugal and the Ukraine. “We have been impressed with the Portuguese government’s grasp of the hydrogen opportunity,” said Chaudhry, and “the other dark horse is Ukraine, which has good solar and wind resources, pipelines into Europe and a vested political interest in becoming resource independent.”

Death throes

Green hydrogen may be the talk of the town, but grey, blue, and even “turquoise” hydrogen still make up a good amount of the talk that’s going on behind closed doors. Many nations will be unwilling to commit to green hydrogen, some lack the resources, some the infrastructure, some the political or entrepreneurial will, and some are waiting, perhaps greedily, for more immediate incentives from trading partners and the market. “There is difference all around the world,” said Wijk, “of where the hydrogen will come from.”

For this reason, many nations will adopt the hybridized approach. Take Kazakhstan for instance, it is a nation the size of Europe with enormous resources, particularly wind and natural gas. Kazakhstan’s central location on the Eurasian landmass makes it ideally situated to export to export to hydrogen hungry nations in both Europe and Asia. Moreover, as Wijk points out, Kazakhstan is already venous with pipelines that can be used to transport their gray-green hydrogen.

In the end though, as Wijk is unafraid to declare, solar and wind will win out. Fossil fuels will simply fail to compete for price on the global market as the century rolls on with sun beating and wind chiming. “I’m not so afraid,” say Wijk “in the end solar and wind will out-compete.”

In the interim, the play of these opposites, renewables and non-renewables, future energies and “traditional” energy sources, will ensure a dynamic geopolitical scramble. While future generations will scoff derisively at the idea that fossil fuels could ever be deemed more “traditional’” than sun, wind, and water, living generations know that some traditions die hard.

Nevertheless, this scramble for the green hydrogen economy looks set to play out on a global scale between resource-rich nations with existing infrastructure, before the race devolves into regional markets wherein those who have solar and wind will compete for exports to neighbours who have not.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.