Short-term symptoms

The 2019 coronavirus outbreak has disrupted the global PV supply chain. China, the largest manufacturing hub for solar products, has postponed factory openings in many regions, as it has been hit by logistical hiccups, staff shortages, and delivery delays. Manufacturers in some Chinese provinces are running under capacity, while those overseas are facing the same situation.

Wafer size transition in the midst of Covid-19

As the Covid-19 pandemic takes the world by storm, global supply chain operations remain disrupted, and solar exhibitions that were held in the first quarter of the year saw fewer manufacturers displaying their latest products.

N-type uptake under Covid-19

As p-type mono cell efficiencies edge closer to their limits, n-type cells are increasingly being recognized as next-generation technologies, writes PV InfoLink analyst Amy Fang. Manufacturers have focused their research and development efforts in recent years on the creation of commercially viable pathways for heterojunction (HJT) and tunnel-oxidized passivated contact (TOPCon) cells.

Module prices plunge as Covid-19 hammers demand

Some European countries and emerging markets are now showing signs of slow recovery, as the Covid-19 pandemic brought overseas markets to a shuddering halt in late March. However, demand is expected to remain weak through the beginning of the third quarter, writes PV InfoLink’s Amy Fang, as it will take time for overseas markets to snap back. Meanwhile, the Chinese market is again busy with the June 30 installation rush, as the government has left tariff timelines unchanged up to the middle of May.

As countries reopen, market recovery begins

As the Covid-19 pandemic gradually eases, countries around the world have slowly begun to relax lockdown measures. Some countries have also launched varying types of economic stimulus to support the solar sector. In contrast to others, the Chinese market is stable, as the country has had some success in controlling the virus.

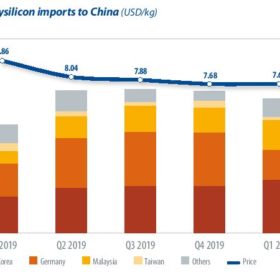

Consolidation continues for polysilicon makers

While mono-grade polysilicon prices did not decrease much in the first quarter owing to stable demand, multi-grade fell to record lows as its market share diminished. During the second quarter, writes PV InfoLink senior analyst Cooper Chen, the market saw excessive supply. Monocrystalline manufacturers have been running at full tilt and bringing new capacities online as scheduled, while the pandemic rages on overseas.

Bigger and better: Technology

The SNEC 2020 PV Power Expo opened on Aug. 8 in Shanghai. Unlike previous editions, the world’s largest solar trade fair was mostly attended by Chinese participants this year due to the Covid-19 pandemic. While the trade fair used to offer insights into global market trends, volumes were low this year due to a buyer/seller standoff amid rising prices caused by the recent accidents at polysilicon plants in Xinjiang. Also, there was little change in technologies. PV InfoLink’s Corrine Lin offers insights into cells and modules at SNEC 2020.

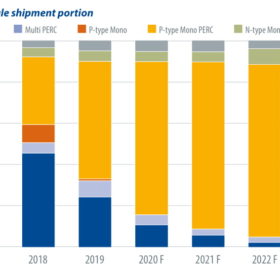

N-type market growth

Several manufacturers recently brought average mono PERC cell efficiency to 22.5%, and efficiencies will likely go beyond 22.6% in the second half of this year. This suggests that p-PERC cell efficiency could be brought closer to that of n-type, making it more difficult for n-type cells to compete in the increasingly challenging market. Taking costs and market conditions into account, most manufacturers have slowed their capacity expansion plans, leading to a gap between actual output and production capacity. PV InfoLink’s Wells Wang sheds some light on n-type trends in 2020.

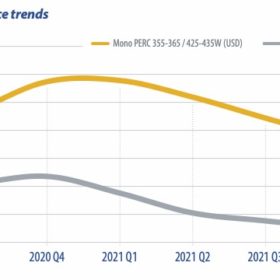

Prospects for bifacial and large-format products

The pandemic and accidents at polysilicon labs in China’s Xinjiang region put PV manufacturers under pressure to maintain production this year, while slowing cell and module R&D. After half-cut and multi-busbar becomes commonplace, manufacturers will continue to explore the high-density assembly methods that emerged last year, as well as n-type cells. But the market is also shifting to large formats, and the share of bifacial products is growing this year. As sizing up modules can bring immediate returns, PV InfoLink’s Amy Fang expects the PV industry to prioritize the development of large formats and bifacial products next year.

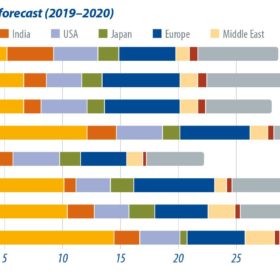

Solar set to shine in a post-pandemic world

The world is still combating Covid-19, with Europe now impacted by a second wave of the virus. While the market reported delays for a few projects, the impacts on the PV sector remain unclear. But if the world fails to curb the Covid-19’s spread, governments may be forced to reintroduce strict measures, thereby sapping PV demand. PV InfoLink’s Mars Chang expects module demand to hit 126 GW by the end of this year.