From pv magazine Germany

The PV industry in Germany is struggling, with company bankruptcies piling up, reflecting a trend seen across all sectors. According to Deutsche Wirtschaftsnachrichten, the number of bankruptcies in the third quarter of 2024 reached a high not seen since 2010, mainly due to self-inflicted problems and ongoing price declines.

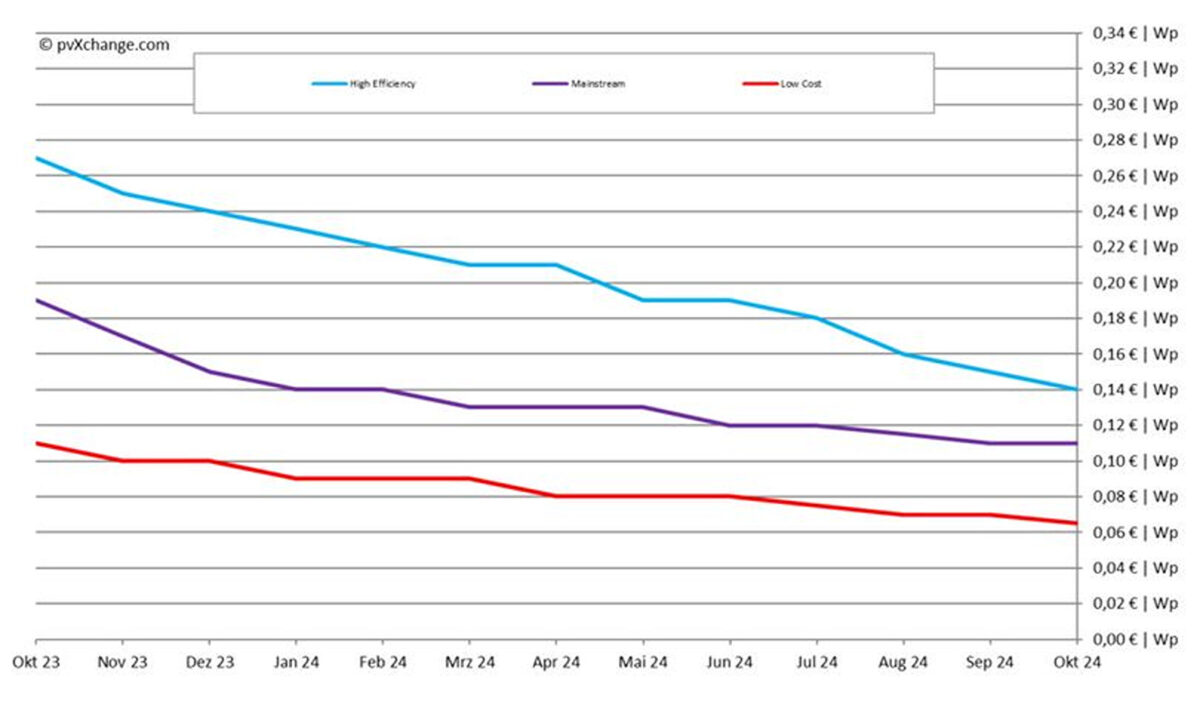

This month, the price declines mainly affected TOPCon modules in the higher performance classes, which fell by an average of €0.010/W, while prices for other module classes remained mostly unchanged. Many suppliers are still under pressure, devaluing even popular brands just to boost sales.

However, the past six to nine months show this strategy isn't necessarily working. Despite lower prices for components and turnkey systems, demand and sales figures haven't seen a corresponding increase.

There is still strong reluctance to buy, particularly in the residential segment, due to uncertainty about long-term economic conditions and individual incomes. Meanwhile, the cost of living continues to rise, despite weaker inflation, along with increasing authorization times from administrations and authorities.

Recent interest rate cuts have failed to improve the investment climate. New installations across Germany and Europe seem to be stagnating at levels seen in recent months. While the growing C&I segment has partially offset the decline in large systems and small government-subsidized systems, it has not yet compensated for the drop.

If we look at why the number of PV installations is declining even for large roof and ground-mounted systems, even though the situation should have improved and the bureaucratic hurdles should have been reduced, we can see the discrepancy between expectations and reality. It is not enough to simplify the rules if there is not enough staff to process the flood of project applications. For example, the time between submitting an application to the network operator and receiving network approval has increased significantly in many regions instead of shortening. If the capacities in the low- and medium-voltage network are also exhausted and additional transformers or even substations have to be built, a major project can be delayed indefinitely.

And now we come to the point where companies' existence is at risk. Especially for medium to large projects, the planning lead time is often immense, and staff and sometimes materials have to be prefinanced. However, the risk all too often lies with the project developer, because banks cannot do much with the current business models beyond the legally guaranteed remuneration. They need planning security, which is rarely provided, neither when building the system nor when later selling the energy generated by it. The sword of Damocles of the temporary curtailment of the photovoltaic system now hangs over everything. If the periods of negative electricity prices continue to increase in the future, there is a risk of economic damage.

The decline in PV installations, even for large rooftop and ground-mounted systems, highlights a gap between expectations and reality. Simplified rules are not enough if there isn’t enough staff to process the flood of project applications. In many regions, the time between applying to network operators and receiving approval has increased. When low- and medium-voltage network capacities are exhausted, and new transformers or substations are needed, projects can face indefinite delays.

Companies now face existential risks. For medium to large projects, planning lead times are immense, and prefinancing for staff and materials is common. However, project developers often bear the risk because banks require planning security, which is rarely available during construction or energy sales. The possibility of temporary photovoltaic system curtailment threatens further economic damage, especially if periods of negative electricity prices increase.

The market’s recent rapid growth is now reversing, as companies that expanded too quickly struggle. The PV industry has always moved in waves, with booms followed by downturns. The boom of 2022 and 2023 brought a surge in installations and prices, but now prices are sharply correcting, with expectations of returning to a more modest growth trend.

This market consolidation mirrors what occurred in the early 2010s. Companies with overly high expectations are collapsing, having failed to remain flexible and adapt to changing conditions. Firms must prioritize flexibility, investing in qualified personnel to manage increasing market complexity rather than chasing every deal or focusing on short-term, low-competition opportunities.

Insolvencies are rising across the photovoltaic market. Planners and installers are struggling with slow order inflows, investor hesitation, and delays that cause fixed costs to skyrocket. Wholesalers are weighed down by excess inventory, while competition among suppliers – especially across borders – is becoming self-destructive. This consolidation wave will likely affect some producers, including those in China.

However, the positive side of market consolidation is that stronger, more innovative companies will survive. Once the market stabilizes, communication and installation quality should improve. It's time to send positive signals to the market and the public to boost investment, restore confidence in future technologies, and improve the order situation.

Price points differentiated by technology (as of Oct. 15, 2024):

About the author: Martin Schachinger has studied electrical engineering and has been active in the field of photovoltaics and renewable energy for almost 30 years. In 2004, he set up the pvXchange.com online trading platform. The company stocks standard components for new installations and solar modules and inverters that are no longer being produced.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.