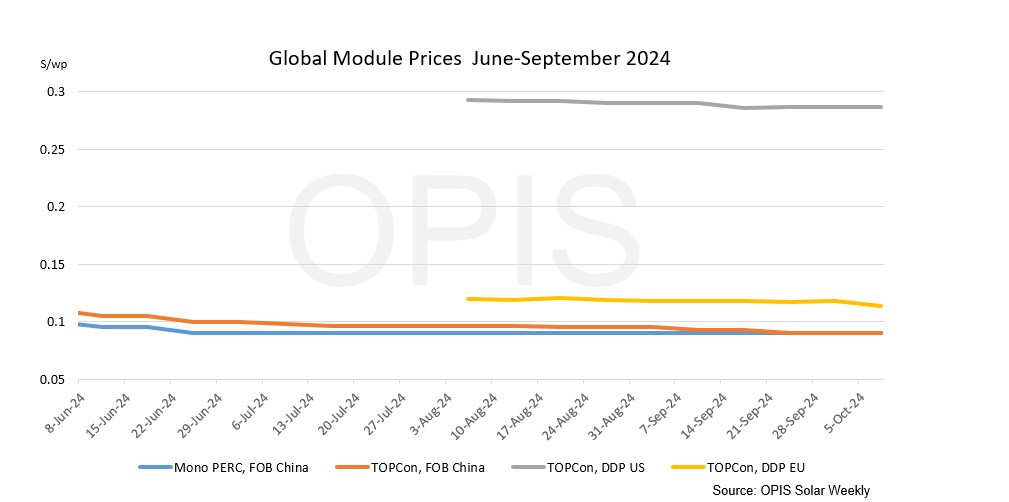

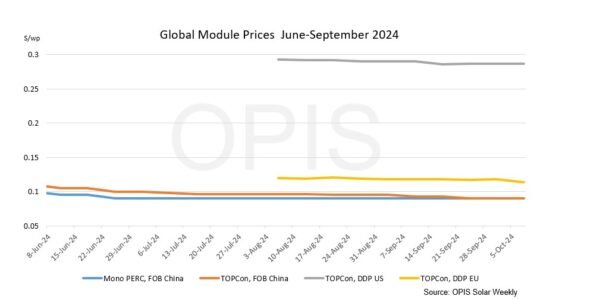

FOB China: The Chinese Module Marker (CMM), the OPIS benchmark assessment for TOPCon modules from China was assessed at $0.090/W Free-On-Board (FOB) China, stable amid unchanged market fundamentals. Although the China market had re-opened on Tuesday after the Golden Week holidays from October 1-7, trading activity remained subdued with most market players expecting buying activity to pick up towards the end of the week.

Tradable indications were heard at $0.085-0.09/W FOB China from Top 10 module sellers. There were expectations of prices weakening in the coming weeks as module sellers started to clear their inventories in October and rush for final sales orders before the end of the year. Operating rates in October were expected to remain high during this period, a market source said. China could produce about 50 GW of modules in October, up from about 49 GW in September, the source added.

DDP Europe: TOPCon module prices slightly dropped week-on-week. OPIS assessed the average price at €0.104 ($0.113)/W, with indications still ranging between a low of €0.090/W and a high of €0.122/W. According to market participants, DDP Eastern Europe TOPCon pricing would vary between €0.090/W and €0.130/W. European sources reported TOPCon module pricing for panels ‘Made in Europe’, between €0.20/W and €0.30/W.

Freight rates for the China/East Asia-North Europe Ocean route were seen at $5,074 per forty-foot equivalent unit (FEU). This corresponds to $0.0120/W, stable week-on-week.

DDP U.S.: The spot price for TOPCon modules DDP U.S. remained flat this week at $0.287/W, with forward indications showing a slight bump in the new year to $0.297/W and $0.300/W in the second quarter of 2025. The market continues to watch for policy news this fall, as new anti-dumping rates and proposed Section 301 tariffs on Chinese polysilicon and wafers could nudge prices higher.

One large North American solar developer said the proposed Section 301 tariffs on Chinese polysilicon and wafers could be more impactful than the 50% rate suggests, given they would apply to both early steps in the supply chain, and join a litany of other applicable duties. The U.S. Trade Representative is fielding comments on the matter through October 22.

The same source suggested a 15-cent premium could be applied to domestic modules for the residential and commercial & industrial (C&I) sectors, while the utility-scale market might only bear a 2-to-3-cent bump over imports. The domestic content bonus will be a much higher value-add for smaller projects, where capex represents a higher percentage of overall costs, the source said.

OPIS, a Dow Jones company, provides energy prices, news, data, and analysis on gasoline, diesel, jet fuel, LPG/NGL, coal, metals, and chemicals, as well as renewable fuels and environmental commodities. It acquired pricing data assets from Singapore Solar Exchange in 2022 and now publishes the OPIS APAC Solar Weekly Report.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.