From pv magazine 12/2021

China’s PV demand is expected to reach as high as 70 GW next year. InfoLink projects that global module demand will range between 196 GW and 212 GW, up more than 20% on 164 GW this year. In the meantime, the rising deployment of solar+storage will accelerate steady solar growth. On the storage side, InfoLink predicts that the total number of homes equipped with solar will pass 11 million, while storage will hit 1.5 million, across four of the leading markets Germany, Japan, Australia and the United States by the end of the year.

Cross impact

The international trade situation and China’s power rationing pose major threats to 2022 deployments. If China relaxes power rationing next year, the pace of PV module price decreases will be subject to polysilicon prices. Polysilicon manufacturers will work toward bringing new capacity online as scheduled, amid high gross margins. Against this backdrop, annual polysilicon production is expected to reach 700,000 MT, which is enough to supply approximately 255 GW of end-user demand.

However, vertically integrated companies continue to ramp up their in-house wafer capacity, while new wafer players such as Gaojing and Shuangliang are also expanding. Large volumes of new wafer capacity will push up demand for polysilicon, and the newly installed furnaces require three to six months to ramp up fully. Therefore, the supply of polysilicon is expected to remain tight in the first half of 2022, with prices decreasing too slowly to ease high PV module cost pressures. Polysilicon prices are expected to hover around CNY 190/kg ($26.35/kg) by mid-2022. If the United States continues its sanctions against Xinjiang, polysilicon prices in regions outside of China may be slightly higher.

Polysilicon prices are projected to decline quarter on quarter, as polysilicon supply grows. If module prices remain high, PV plants that have halted installation will try to postpone as long as possible to secure better module prices. In light of this, module prices and overall demand will impact each other next year. If module prices decrease markedly, overall module demand will increase.

While capacity expansion continues across the supply chain, uncertainties caused by power rationing and international tensions will lead to low module orders for the first quarter of 2022. Consequently, module prices, which stayed at $0.28/W to $0.29/W, finally showed signs of decline in November. Meanwhile, prices for other components such as glass also began to slip. It’s expected that a slow downward trend in module prices will begin in the first half of 2022.

Trade risks

In early November, the U.S. Department of Commerce rejected anti-circumvention petitions, providing breathing space to manufacturers with capacity in Southeast Asia. If anti-circumvention is no longer an issue next year, capacity expansion projects in Southeast Asia will continue as planned, with 15 GW of capacity addition expected for both the PV cell and module segments.

In addition to the Xinjiang issue, which has caused polysilicon prices to move unsteadily, the U.S. Withhold Release Order (WRO) also put Southeast Asia-based businesses on watch. Thus, production lines in the region are not likely to return to full capacity utilization until this uncertainty is overcome.

Southeast Asia aside, wafer, cell and module capacity expansions are concentrated in China. Because of the rapid shift to large-format products, global wafer, cell, and module capacity are each set to grow more than 140 GW this year. The cell segment saw the largest volume of additional capacity, reaching around 180 GW. Given new production lines are more competitive, capacity across the supply chain will continue to grow next year, with the wafer and cell segment each adding 100 GW of new capacity.

The combined capacity of wafer, cell, and module will outgrow end user demand and surpass 350 GW by the end of the year. Production costs of conventional format modules are higher by CNY 0.01/W than the large-format ones, and as sales of conventional format modules are low, older production lines will be eliminated next year. However, those installed for PERC around three to five years ago may simply be left idle.

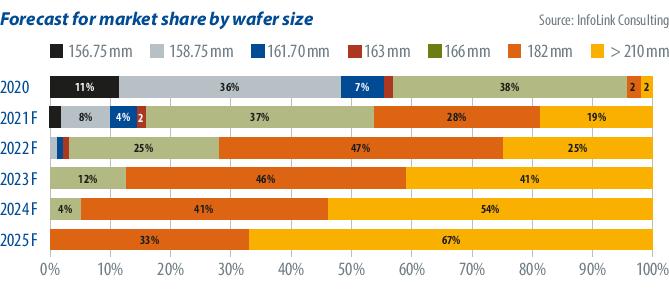

As most manufacturers started production of large-format products with the 182mm format, modules featuring 182mm cells and a power rating of 535 W to

545 W will see the largest share, followed by the 210 mm format. Cell numbers and layout vary across manufacturers. The two formats will together make up more than 70% of next year’s share, while M6 and smaller-format modules will continue to be used in the rooftop sector.

TOPCon vs. HJT

In terms of cell technology, PERC cells began to see profits decreasing to nil due to overcapacity. Meanwhile, manufacturers are expanding tunnel oxide passivated contact (TOPCon) and heterojunction (HJT) capacity, both n-type products. After China successfully localized production of the factory equipment to produce these cell technologies, the required investment per gigawatt has fallen from $35 million to $28 million for TOPCon, and from $62 million to $55 million for HJT this year, a significant reduction bringing them closer to the $22 million/GW required by PERC. It appears that TOPCon capacity additions will reach 20 GW to 30 GW next year, while HJT may see a 15 GW to 20 GW expansion.

As equipment cost reductions will reach a limit, the optimization of manufacturing costs will continue. Metallization cost reductions will remain key next year, while n-type cells will help reduce costs through adopting large wafers. With the combination of large wafers and large module designs, the market is expected to see n-type modules featuring power outputs higher than 600 W.

It seems that prices for TOPCon modules will be $0.02/W higher than PERC modules, which will already be an appealing price point for end users. Therefore, TOPCon will outgrow HJT in terms of capacity and production.

Nevertheless, PERC products are currently the most mature and cost competitive on the market. So, it’s expected that n-type products will stay in the promotion and preparation phase next year, and the market share will grow slowly and steadily from 4% this year to 6% to 7%.

By Corrine Lin, InfoLink

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

3 comments

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.