From pv magazine 03/2021

IHS Markit forecasts that the United States will install more than 20 GW of utility-scale PV installations in 2021, making it another banner year for solar. Notably, the utility-scale segment already has over 11 GW (DC) of projects under construction. Other contributing factors to the growth of solar this year are the transition of coal states to renewables generation in the near-term; states like Illinois, Virginia, Pennsylvania, and Kentucky allhave large PV pipelines in 2021 through 2025. Moreover, continued corporate procurement for PV generation and aggressive net zero goals by large utilities across the country will ensure the maintenance of growth for solar over the next five years.

ITC extension

On Dec. 21, 2020, both houses of Congress passed a large Covid-19 and funding bill that included a two-year extension of the solar Investment Tax Credit (ITC), a one-year extension on wind production tax credits (PTC), and funding for energy research and development programs, among other provisions. The extension of the ITC will likely reshuffle the demand for PV projects from 2022 through 2025 as investors seek to capture the ITC 26 and safe harbor provisions at a price point that is beneficial to their returns. Allowing two additional years for the 26% credit will improve the economics of solar overall, as the credit will now be coupled with a smaller tariff for solar cells and modules (assuming the tariff is not extended).

For the residential market, homeowners across the country had been rushing to secure the ITC 26 by installing solar in their homes in 2020, despite challenges posed by the Covid-19 pandemic. However, the residential segment is more sensitive to tax credits than the non-residential segments. The extension will drive an immediate spike in demand, followed by declines that are correlated to the ITC step-down.

The two-year solar tax credit extension is expected to spur more demand for residential and commercial solar systems in several emerging markets. This means that 2021 will be an important year for residential installers, but consumer demand from 2022 onwards will taper off, as mature markets reach saturation and net metering and distributed solar programs continue to be challenged and modified across the United States.

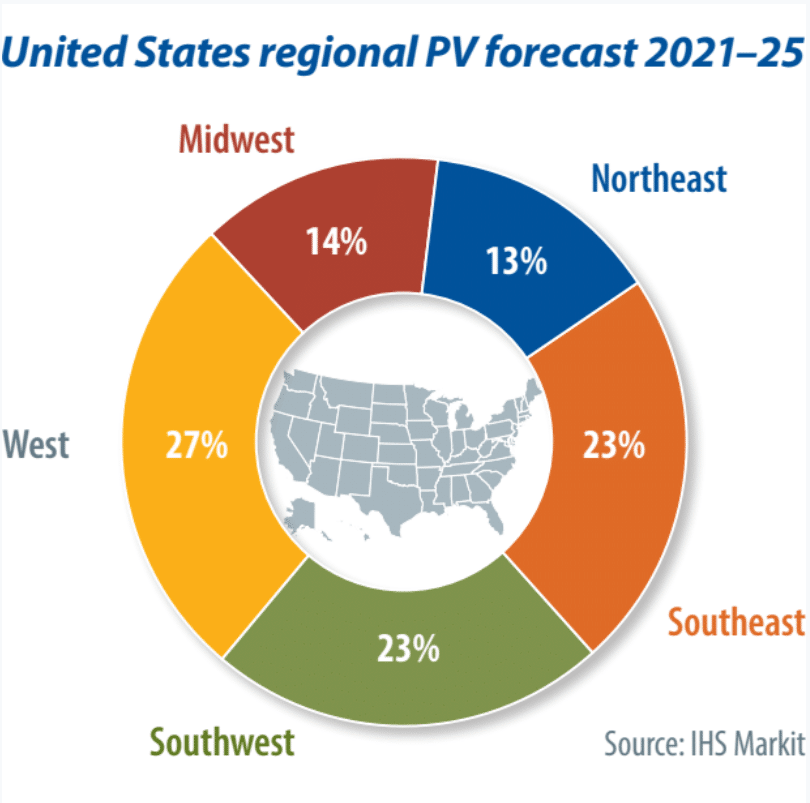

New markets

In 2021, the Midwestern and Southern United States will be responsible for 60% of PV installations in the country. States like Illinois, Ohio, Georgia, Florida, and Texas will contribute to a large portion of installation volumes in these regions. Demand for PV in the Midwest is forecast to be primarily driven by the utility-scale solar market, as utilities seek to comply with varying levels of renewable energy and emissions reduction goals.

Similarly, in the Southeast, large utilities such as Duke Energy, Georgia Power, Dominion Energy, and Florida Power & Light are driving demand for utility-scale solar through cost competitive, voluntary procurement mechanisms. These utilities, among others, have set aggressive net-zero renewable energy generation targets that will require solar PV procurement in the near future. Moreover, utility partnerships with large corporations are driving further demand for utility-scale solar projects.

In the Southwest, IHS Markit forecasts that the utility-scale PV segment will drive demand, with most of the installations attributed to massive PV growth that is expected to continue in Texas through 2025. Although utility-scale installations will dominate the market in Texas, the residential segment also gained momentum in 2020 and will sustain similar levels in the short-term, as consumers take advantage of the extended ITC and utility incentives like rebate programs.

Green goals

Historically, the residential and commercial PV segments have driven most of the demand in the Northeast and will continue to do so. However, due to New York’s aggressive utility-scale goals, the large-scale segment will account for more than half of PV demand in the region. Recently, the state announced 23 utility-scale projects that have a combined capacity of 2.2 GW. Additionally, the New York State Public Service Commission (PSC) has approved construction of a 55-mile transmission line that aims to enhance reliability and speed the flow of energy from upstate NY to the lower parts of the state.

New Jersey, Massachusetts, and Maryland will also help drive most of the PV growth in the Northeastern United States in 2021. Lawmakers across the region have put forth policies that could help PV growth, though some have been more successful than others. Earlier this year, Governor Charlie Baker of Massachusetts vetoed legislation that required the state to achieve net-zero emissions by 2050. More recently, Governor Baker has suggested amendments to the bill and is awaiting a response from the state legislature.

PV policy

IHS Markit forecasts that installations of energy storage projects in the United States will account for more than 5 GW of capacity in 2021. The extension of the ITC will likely improve the economics of solar+storage systems and enable energy storage projects to be co-located with PV to benefit from a reduced tax burden through 2025.

The Federal Energy Regulatory Commission (FERC)’s Order 2222, which was passed in 2020, opens wholesale markets to behind-the-meter energy storage. But it may take longer than expected for this ruling to become a strong market driver. Order 2222 aims to allow distributed energy resources (DERs) to participate in wholesale power markets by bundling together as a single bidding entity. Recently, regional transmission organizations, and other stakeholders, have requested an extension to the order, citing too short of a timeline to implement the ruling.

While the United States will continue to extend its dominance in the storage market, incentives for storage are still lacking in the country, with a standalone storage tax credit not easily guaranteed, as Democrats only control the Senate by a small margin. In the near term, the most consequential federal policies benefiting the energy storage industry will likely be in the form of executive actions.

About the author

Maria Jose Chea is a research analyst with the solar team at IHS Markit. She leads the North America and Latin America research for the Downstream PV Intelligence Services, including the tracking and analyzing of both downstream projects and market policies. Prior to joining IHS Markit, Chea worked in Brooklyn, New York, at a renewable energy financial advisory startup as part of its transaction advisory team.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.