From pv magazine 01/2021

The U.S. House of Representatives passed a bill in September seeking to block imports of goods made in Xinjiang province, China due to forced labor concerns. Xinjiang is a major producer of fossil fuel, and supplies around 20% of the world’s cotton, as well as more than 40% of the world’s solar grade polysilicon. The U.S. government has issued orders barring imports of cotton from the region. According to the bills, the U.S. Customs and Border Protection would be required to treat all goods made in whole or in part within Xinjiang as presumptively banned from entry into the United States within 120 days of the law’s enactment.

Xinjiang solar

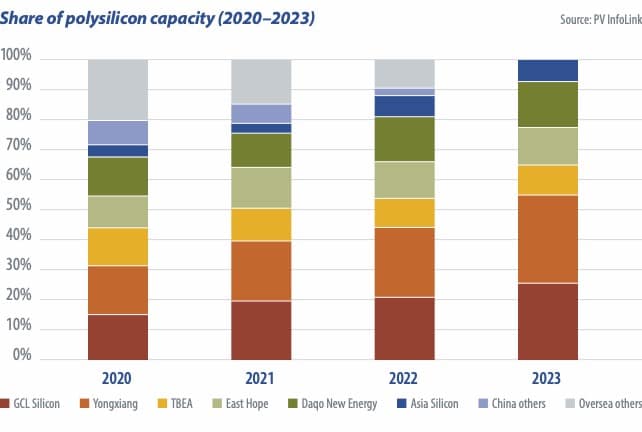

China’s polysilicon capacity will come in at 452,000 metric tons (MT) at the end of 2020. Of this, 237,000 MT – 52.4% of the total in China and 41.7% of the global polysilicon market – is located in China’s Xinjiang region.

The polysilicon production capacities of Daqo New Energy (75,000 MT), TBEA (72,000 MT), and East Hope (50,000 MT, plus 100,000 MT planned) are located entirely in Xinjiang, as well as 46.5% of GCL-Poly’s 86,000 MT total capacity.

China’s mono-Si Ingot capacity reached 182 GW at the end of 2020, but Xinjiang houses less than 20 GW of the ingot capacity. The few lines of cell and module production that remain in the region have been halted already. It is worth noting that two manufacturers with capacity in Xinjiang are listed on the New York Stock Exchange. Daqo plans to raise CNY 5 billion ($773.9 million) for a high-purity semiconductor project with 1,000 MT of annual capacity, and a 35,000 MT solar-grade polysilicon project. It may postpone or build them outside of Xinjiang.

A 42% chunk of JinkoSolar’s 8 GW ingot pulling capacity is in Xinjiang. It had planned to expand this to 14 GW, but may instead add ingot pulling capacity to its Leshan and Xining-based facilities.

Global capacity

In recent years Chinese producers have expanded into parts of western China such as Xinjiang, Inner Mongolia, Sichuan, and Yunnan, where electricity is cheaper, leading to increased concentration of polysilicon capacity.

Yongxiang, Daqo, and GCL-Poly will each ramp up more than 100,000 MT between 2021 and 2022. Others may expand after 2023. Chinese polysilicon producers’ cost advantage will allow them to edge out foreign rivals. The volume of polysilicon imported into China could fall very low as early as 2023.

Potential impacts

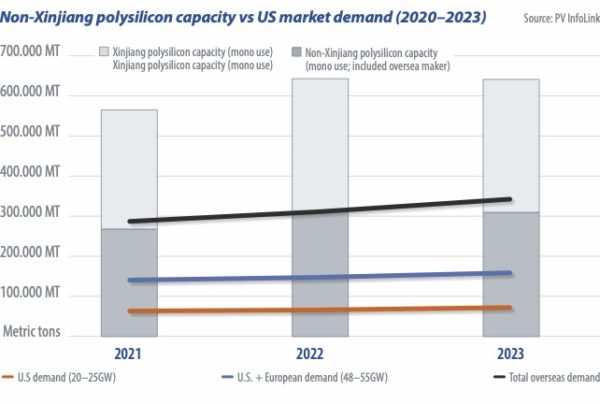

The United States urged Europe to follow suit after its ban on imports of certain goods from Xinjiang. Considering that Europe has imposed trade barriers against other industries before, polysilicon demand is estimated in three scenarios: U.S. demand alone, demand from the United States and Europe combined, and that all non-China customers stop using Xinjiang-produced polysilicon. The estimate suggests that even if the U.S. government and the European Union impose new sanctions, polysilicon capacity in non-Xinjiang regions is enough to fulfil module demand from these two regions.

Under the worst-case scenario, in which overseas markets no longer use Xinjiang-produced polysilicon, non-Xinjiang polysilicon capacity will fall short of module demand. However, it appears unlikely that all overseas markets will stop using products that contain materials from Xinjiang.

Since Europe and the United States would prefer polysilicon produced outside of Xinjiang, manufacturers may have to move production lines to other provinces, unless they can provide credible evidence that they have no part in forced labor practices.

Vertically integrated companies are negotiating contracts with non-Xinjiang polysilicon suppliers in anticipation of bans. Considering that it is highly complex to verify certificates of origin, wafer makers and vertically integrated companies may opt to source polysilicon from non-Xinjiang regions.

This has pushed manufacturers to sign long-term contracts to ensure a certain ratio of non-Xinjiang-produced polysilicon. This year more than 70% of the world’s polysilicon has been booked, and the share of long-term contracts may increase. This trend also prompts big manufacturers to form partnerships, such as the project signed by Tongwei and Trina.

PV InfoLink says mono-grade and multi-grade polysilicon prices will respectively reach CNY 65/kg and CNY 38/kg at the end of 2021. Factoring in labor concerns and trace of origin, suppliers outside of Xinjiang will have an advantage in sales.

Based on the mono-grade polysilicon price of CNY 70/kg, the estimated module price is CNY 1.5/W. As capacity will have grown significantly across the supply chain in the second half of 2021, the market situation may experience a transition period after the June 30 installation rush, sending module prices slowly downward. By then, unsubsidized projects are likely to get off the ground. Large module manufacturers are expected to initiate price wars, forcing wafer, cell, and even polysilicon manufacturers to react promptly.

This article was amended on 18/05/2021 to correct an error regarding wafer capacity located in Xinjiang Province.

About the author

PV InfoLink Senior Analyst Cooper Chen specializes in photoelectrochemistry and solar cells. Over the past seven years, he has been involved in crystalline silicon wafer R&D for solar cell applications. With in-depth knowledge of the solar supply chain and advanced manufacturing processes, he provides market trend analysis and price forecasting for the upstream solar PV segment.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

It would be great if your “worst-case scenario” mentioned the accompanying forced labor, internment, cultural erasion, religious suppression, mass surveillance, and all around exploitation of the Uighur population. You don’t even mention the cause of the sanctions by the US House. However, that doesn’t seem to be important. Perhaps shifting supply chains at a short-term cost will have positive long-term impacts that don’t have obvious economic benefits. It would be great if your magazine had the courage to take a stance on human rights violations and cultural genocide.