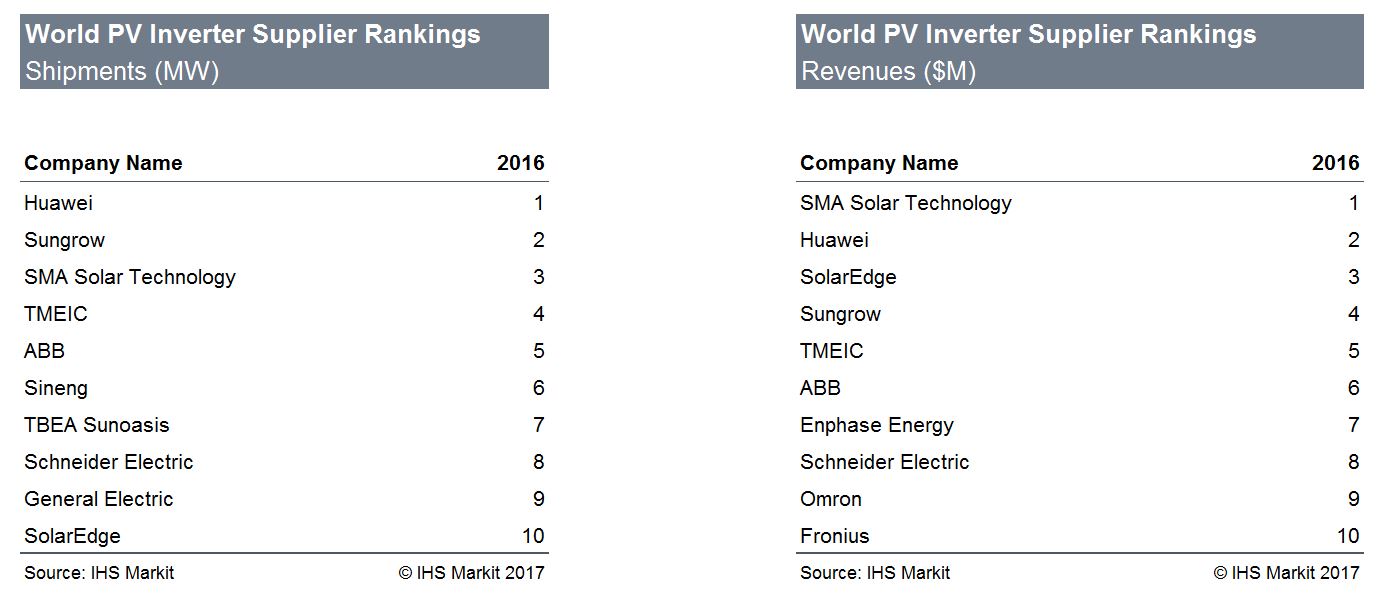

German inverter specialist SMA has clung once again to top spot in the latest IHS Markit Global 2016 PV Inverter Rankings with 14% of all revenue share last year. This figure represents a very slight increase on its 2015 global share despite SMA still being unable to make any significant inroads into the huge Chinese market, IHS Markit solar research manager Cormac Gilligan told pv magazine.

“In managing to post a slight increase in revenue share, particularly in a competitive market with falling prices, and with limited exposure in China, SMA’s performance in 2016 was very good,” Gilligan said.

Hot on SMA’s heels was China’s Huawei, which – just like in 2015 – grabbed the second-highest global share of revenue and maintained top position in terms of shipments. Israeli firm SolarEdge built on a strong 2015 to place third in 2016’s revenue chart (up from fourth place in 2015), with China’s Sungrow in fourth place and Japanese central inverter specialist TMEIC in fifth place.

“Both SolarEdge and TMEIC have had an excellent year,” said Gilligan. “SolarEdge maintained its strong position in the U.S. residential sector while also continuing to operate a very broad customer base in residential and small commercial markets globally.” TMEIC built upon its leading position in Japan’s utility scale sector to claim large revenues in the U.S. and India, the IHS Markit analyst added.

Another noteworthy performance in the revenue ranking was that of U.S. microinverter specialist Enphase which, despite offering a seemingly narrower portfolio of products in fewer markets was still able to claim seventh place in the ranking. “The module level power electronics (MLPE) space has been challenging in 2016, but even in these conditions Enphase has performed well in its key market of the United States while continuing to expand in Europe and Australia,” Gilligan stressed.

The top ten also saw the return of Austria’s Fronius, which last troubled the charts in 2012. “Fronius has experienced a similar story to SMA,” said Gilligan. “The company has completely updated its portfolio of products and as a result has done a good job of gaining market share in Europe, the U.S. and Australia.”

Shipments show China influence

The World PV inverter supplier rankings in terms of MW shipments was topped by Huawei, with Sungrow in second place, SMA third, TMEIC fourth and Swiss firm ABB in fifth place. However, the most prominent difference between the two charts was the presence of Sineng and TBEA Sunoasis in sixth and seventh place respectively. These Chinese firms have a strong domestic presence that helped them to edge out some of the more globalized suppliers.

“For ABB, India remained a leading market in 2016, while Schneider Electric [eighth place] again benefited from being a global multinational with a standout performance in India, France and other European markets.”

The lopsided nature of China’s domestic solar demand evident in 2016 will again rear its head this year, Gilligan said, forcing many leading Chinese suppliers to target the Indian solar market in the second half of this year as their domestic market slows down. “We forecast that India will see around 9 GW of inverter shipments across all segments in 2017.”

Other notable trends to look out for this year include the ongoing adoption of 1,500 V inverters, particularly central inverters, although India may lag on this front due to domestic manufacturing requirements. “Companies such as ABB, Schneider Electric, TMEIC, Ingeteam and Hitachi have set up their fabs in India largely for 1,000 V, and may not be ready this year to transition to 1,500 V,” Gilligan revealed.

In the central inverter segment, the big trend is the increasing size of the units, as evidenced by SMA’s forthcoming 5.5 MW turnkey central inverter. This trend is also beginning to be mirrored in the string inverter sector, where the average power rating offered by most leading suppliers is rising. “We are now seeing string inverters offered at 60 kW through to 80 kW and even 100 kW,” Gilligan said. “This gradual ramp up of power offers lower dollars per watt, and is an important trend throughout the sector.”

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

2 comments

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.